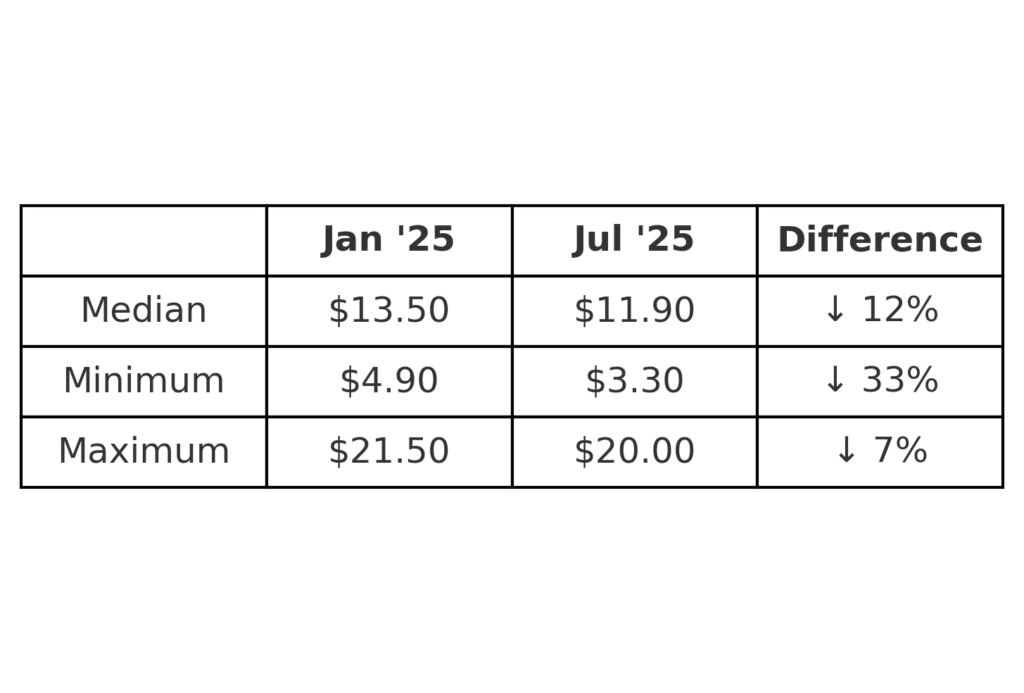

Medicinal cannabis flower in Australia is now available to patients for as little as $3.30 per gram, with honahlee co-founder Tom Brown cautioning that the downward price trend raises serious questions about the viability of domestic cultivation.

That figure sits within a broader pricing shift: 39% of all flower products are now priced below $10 per gram, compared to 27% in January.

Speaking at A Cannabis 2025 in Melbourne, Brown clarified that the $3.30 figure applied to fully packaged products — not wholesale — and that it was already on par with the bulk sale prices being targeted by some Australian growers.

"We know some Australian cultivators are aiming to sell their product in bulk at $3.30 before packaging," he told attendees.

"It's hard to see where Australian cultivation is going to go in terms of API (Active Pharmaceutical Ingredient)."

Brown's findings build on honahlee's previous market update in February, which identified a comparable decline in flower pricing.

He said the most pronounced change over recent years had taken place at the lower end of the pricing spectrum.

"When I last presented this slide, there were 23 SKUs at less than $6 a gram to the patient. Now there are 51," he said.

"In January, 27% of flower products were priced under $10 a gram. Six months later, that's up to 39%."

Although the overall number of SKUs continues to climb, growth in flower products has slowed considerably.

Flower SKUs jumped 72% in H2 2024, but that figure dropped to just 11% in H1 2025 — a deceleration Brown attributed to a market he described as "oversaturated."

Vape cartridges followed a similar pattern, with growth also tapering. H1 2025 produced 10 new vape SKUs — an 8% increase — after a 92% surge in H2 2024.

Pastilles posted the strongest relative growth of any dosage form, rising around 75% in H1 2025 — approximately 51 new SKUs — with more than 10 additional products already listed as coming soon and further additions anticipated.

Concentrates came next, growing 71% in H1 2025, though that amounted to only five new SKUs, while oils rose 5% with roughly 12 new additions.

Brown also drew attention to a new oil product designed for use as a drink or food additive, with the product claiming enhanced absorption.

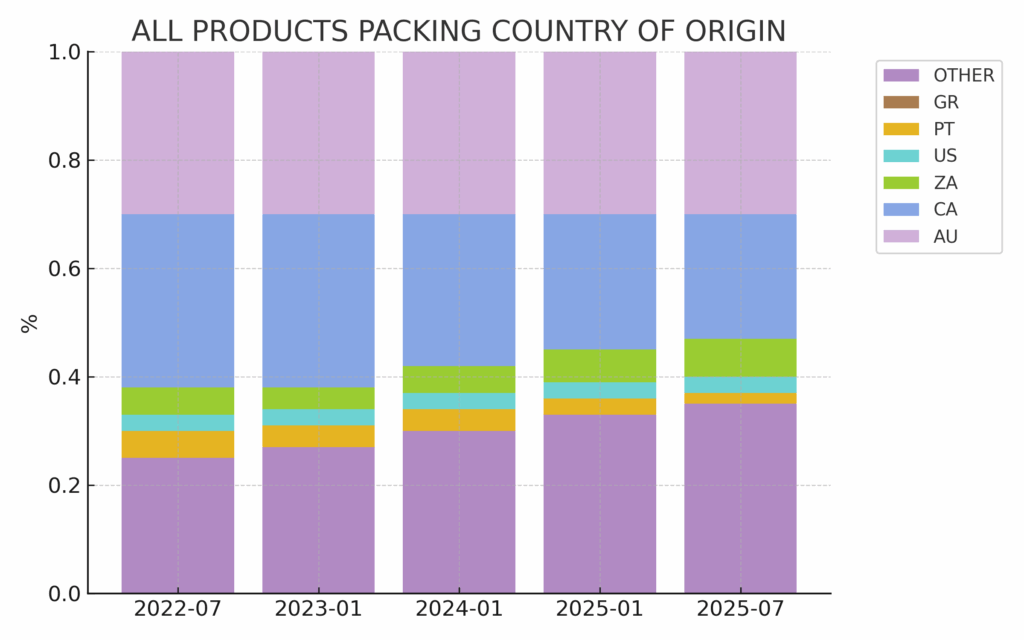

On country of origin, Canada remains the dominant API source, supplying around 45% of the market, with Australia accounting for approximately 26%.

Thailand has also entered the picture as an API source, with 24 listed products plus several others known to originate there that have not been formally recorded.

One bright spot for the domestic industry, Brown noted, was that Australian packaging continued to grow — from 58% of all products in January to 65% in July.

“This does indicate continued growth of local GMP manufacturing, which is great for the local industry and economy,” he said.

Turning to terpenes, Brown expressed frustration with the current state of the market, pointing to unreliable product data and a lack of verification.

"In an overcrowded market with little differentiation, reporting terpenes from batch to batch and actually being able to verify your claims can actually make you stand out," he said.

"Practitioners have more incentive to prescribe products that have a validated terpene profile and patients are searching for terpene profiles consistently [and] talking to their practitioners about what terpenes are in their products.

"The total percentage of products with terpenes measured has decreased from about 23% to 21% since January… [and] 65% of products that list terpene claims don't have certificates of analysis to back them up."

Looking ahead, Brown forecast growth in concentrate products, noting that suppliers are already working to educate prescribers and draw attention to potential advantages over vape cartridges.

"Practitioners are starting to recognise that non-vape concentrates are really no different to vape carts they're already prescribing – and in many cases may offer better medicinal benefits due to factors like terpene profile or content," he said.

He added that as suppliers seek to differentiate through minor cannabinoids and terpenes, established players would face increasing pressure to provide greater transparency.

Separately, Penington Institute's Rhys Cohen said in an interview that medicinal cannabis unit sales in Australia grew 106% year-on-year in 2024, with more than 3.7 million units sold in the second half alone, bringing the annual total to 6.6 million.

He also warned against over-relying on SAS-B prescribing data, noting that Authorised Prescribers now account for "90% of units sold in this market."

NostraData general manager Nick Biggs said price compression was also visible at the pharmacy level.

“We are getting a little bit of compression on margin as well,” he said.